Dhaturi, a dusty village in Haryana some 54 kilometres from the national capital, is like any other hamlet in North India: a cluster of half-plastered, concrete buildings housing kirana stores; semi-paved streets, on which buffaloes saunter, flanked by thatched huts; a sleepy market; and huge swathes of agricultural fields that bear black marks of recently burnt stubble. Dhaturi,哈里亚纳邦的一个尘土飞扬的村庄约54公里的首都,就像任何其他哈姆雷特在北印度:一群half-plastered,混凝土建筑住房商店拉;semi-paved街道,水牛漫步,两侧的茅屋;一个昏昏欲睡的市场;和巨大的农业领域,最近烧麦茬的黑点。

\n

But unlike many other Indian villages, Dhaturi may be in the midst of a remarkable transformation after the government’s radical demonetisation<\/a> drive on November 8. A transition to a digital way of life has begun, and Suresh Pal is at the vanguard of this change. In his small photo studio, Pal doubles up as a retailer for Payworld<\/a>, an electronic transaction processing platform, helping people open an assisted mobile wallet<\/a> account. “Even those without smartphones can use the wallet,” he says.

\n

\nThe Village Logs In <\/strong>

\nPayworld, which had over 100 million users and 1 lakh retail touch points across 630 cities and 80,000 villages till the first week of November, has seen a 25% jump in new users — mostly from rural and semi-urban areas — over the last two weeks. “What we couldn’t achieve during the last nine years was facilitated instantly by Narendra Modi,” gushes Payworld chief operating officer Praveen Dhabhai. “Over 93% of people in rural India have not done any digital transactions. So the real potential lies there.”

\n

\n\n\t\n\t

\n

\n\n\t\n\t

\n

Dhabhai is not the only one rushing in to cash in on an opportunity to take digital payments to rural consumers post demonetisation. ItzCash<\/a>, a digital payments company founded in 2006, too is eyeing a larger share of the rural wallet. While most players, including Chinese ecommerce major Alibaba-backed Paytm<\/a> and Snapdeal-owned FreeCharge<\/a>, are catering to the top 10% of India, ItzCash plans to keep its focus on Bharat where roughly 66% of the country resides, says managing director of ItzCash Naveen Surya. The company, with an omni-channel presence through outlets, mobile wallets and cards, is present across 3,000 towns and cities, and claims to have seen a 40% spike in transaction volumes since November 8. “Over the next few quarters, most of our growth would be fuelled by Bharat,” he says.

\n

\n\n\t\n\t

\n

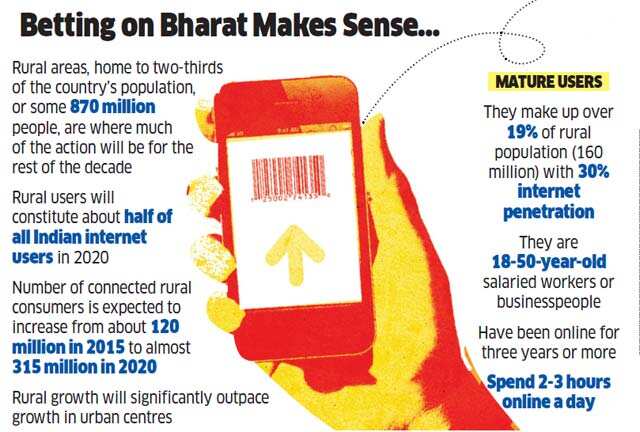

\nRural India, or Bharat, indeed looks like a land of golden opportunity for marketers, including mobile wallet players. Reason: home to about 870 million people, the countryside will be in the thick of action for the rest of the decade, according to a recent report by management consultancy firm BCG. Titled “Rising Connected Consumer in Rural India”, BCG predicts that rural users will constitute about half of all Indian internet users in 2020. While the number of connected rural consumers is expected to increase from about 120 million in 2015 to almost 315 million in 2020 — a compounded growth of almost 30% a year — rural growth will significantly outpace growth in urban centres. And what’s driving the rural growth, adds the report that was published in August, are cheaper mobile handsets, spread of wireless data networks and evolving consumer behaviour.

\n

\n\n\t\n\t

\n

\nAfter Demonetisation <\/strong>

\nNow, there’s the demonetisation effect. Sohan Ram, a roadside vendor selling bread pakoras, noodles and tea from his small makeshift shop at Kurar village in Haryana, is getting ready for a cashless future. He says that although the highest priced product he sells is under Rs 50, mobile wallets ensure that users pay up every rupee, which many of them usually skipped citing paucity of loose change. “Now the ones with mobile wallets can’t make an excuse,” he grins.

\n

\n\n\t\n\t

\n

\nJust a stone’s throw from Ram’s stall is a kirana store. Kishore Chand, the proprietor, dithered for the first few days after demonetization. He thought the government might roll back the move and cash would still continue to be the main medium of payment. But when business dried up as people ran out of cash, 52-year-old Chand quickly installed a cardswiping machine and downloaded MobiKwik, an online payment system. “It’s better late than never,” he says. Although he faced teething problems in the first two days in understanding the technology, he’s now comfortably making transactions.

\n

\n\n\t\n\t

\n

\nIt’s users like Ram and Chand who give hope to the mobile wallet industry, which is projected to jump from Rs 154 crore in fiscal year 2016 to Rs 30,000 crore by 2022. This means a corresponding jump in the value of mobile wallet transactions: from Rs 20,600 crore to Rs 55 lakh crore during the same period, according to a recent study by Assocham-RNCOS titled “Indian M-wallet Market: Forecast 2022.”

\n

\n“From a local cycle shop owner to a sugarcane juice seller to even a temple priest, all have started using mobile wallets,” contends Bipin Preet Singh, cofounder of MobiKwik.

\n

\n\n\t\n\t

\n

\nFounded in 2009, MobiKwik claims to have over 40 million users, and a merchant network of over 2.5 lakh. The company, which was founded in 2009, has seen the most astonishing growth in its user base after November 8: over 5 million in just two weeks.

\n

\n\n\t\n\t

\n

\n“Before demonetisation, wallets were an option. Now they are a need,” says Singh, whose company is increasing its ground staff strength from 1,000 to 12,000 to enrol local merchants for wallet payments. But what Singh also plans to do — and he claims to be a game-changer — is reach out to the next wave of internet users in rural India: young homemakers, who are already online but spend a few minutes surfing the net, constitute over 36% of rural internet users. “If the size of the group is massive, the potential it has is gigantic,” says Singh.

\n

\n\n\t\n\t

\n

\nSuch growth potential can’t be taken for granted, though. Just a few kilometres from Dhaturi, in the neighbouring village of Lalheri Khurd, lives Rampal Narwal, a 55-year-old agriculturist for whom cash has always been king. And he’s in no mood to transact digitally, despite boasting a Motorola smartphone with a 3G connection. Reason: the fear of technology and the unknown.

\n

\n\n\t\n\t

\n

\n“My money can vanish. It’s best to keep it at home,” he says. Why then does he have a smartphone if he just wants to use it to make calls? “Ask my son. He bought it,” snaps Narwal, who in turn is interrupted by his teenaged grandson Sohan. “My father has a Facebook account but the internet doesn’t work properly,” he says, adding that the phone doesn’t have any other app. Not even Paytm. “I have seen its advertisement on TV,” he smiles.

\n

\nNarwal is bemused to see people scrambling to use mobile wallets and debit cards. Ask him about life after demonetisation, and the old man gives a clear-cut reply: “I still use cash, and will always use cash.” Keeping Narwal company is Umesh Dalal, another agriculturist in the adjoining Ramnagar village. Dalal’s biggest argument in persisting with the old way of life is mindset: “Why should I go cashless? How will it change my life?” Sitting next to a huge Jio signboard, Dalal checks his WhatsApp messages on his Micromax Canvas mobile. “There is much merit in transacting only in cash,” he says.

\n

\n\n\t\n\t

\n

\nThe Cashless Cow <\/strong>

\nAs India takes a step towards building a cashless economy, it’s becoming clear that the biggest challenge to Narendra Modi’s vision for a cashless country will come from Bharat, thanks to erratic internet connectivity, poor smartphone penetration — 30%, says CyberMedia Research — coupled with die-hard habits of relying on cash for transactions.

\n

\nExperts contend that the government’s headlong push for a cashless India may be too much, too soon. While the primary goal should be to ensure that everyone has a bank account, and all banks should make it easy to transact digitally, the reality is that many smaller banks do not offer digital banking, says Jessie Paul, founder of Paul Writer, a marketing advisory firm. As far as mobile wallets are concerned, she points out, there are three major issues. First is cost. There is a fee to transfer money to the wallet, and then from wallet to merchant. The second issue is trust. Fear of fraud is high for any digital tool. And there’s reliability; can internet players ensure that there will be 100% uptime of the network?

\n

\nCompounding matters is another problem: when a person doesn’t consume frequently because of paucity of money for impulse purchases, the existing mode of payment, cash, becomes more convenient. “Currently there is no reason for a person to abandon cash and end up paying additional transaction fees to spend their hardearned money,” says Paul.

\n

Nobody understands the power of cash better than Sridhar Gundaiah, founder of StoreKing<\/a>, an assisted ecommerce platform. There may still be some time before India is ready to do a large part of its transactions in plastic money, and demonetisation seems to ignore that, he reckons.

\n

\n“The beauty of cash is that it just works,” says Gundaiah, who follows a unique business model of allowing people to purchase using cash, albeit using ecommerce. The neighbourhood retailer, armed with a tablet and an internet connection, assists customers choose products from StoreKing’s online shopping platform, and the payment is made in cash.

\n

\nAsk him why people in rural India are not shopping online, and Gundaiah lists out a bunch of irritants: every village does not have a pin code, which makes deliveries difficult, low literacy levels, English language barrier and lack of trust in the internet. “Over 85% of the population has no access to debit and credit cards and half of the population is not reachable by traditional courier services,” he says. So, despite having the money and the intent, people in small towns and villages are unable to shop online.

\n

\n\n\t\n\t

\n

\nAnd even if people in rural areas are using mobile internet, it doesn’t mean they are in a mood to transact online. Gundaiah says that among rural users, the primary reason for accessing the net is entertainment, followed by communication and social networking. “We have tapped the rural population with assisted commerce,” he says, adding that he hopes to reach 500 million people in the next couple of years. “There is no way a Flipkart or an Amazon can reach the interiors like we can.”

\n

\nRetail analysts maintain that the task to digitise rural India might be challenging, but not impossible. Saloni Nangia, president of retail consultancy firm Technopak Advisors, says for a large majority of rural Indians, both banking and internet are a new experience. So it’s natural for them to fear both. “There is a huge fear of the unknown, especially when it comes to money,” she says.

\n

\nWhile conceding that there would be hitches in making the transition, Nangia believes that a start has to be made somewhere. She points to the initial scepticism around Aadhaar when it was introduced way back in 2009. But within seven years the unique identity project has enrolled 1.07 billion people, or about 88% of the country’s population. “The focus should be on educating and spreading awareness,” she says.

\n

\nMobile wallet players, for their part, are already on the job. Taking the lead are the likes of Praveen Dhabhai of Payworld, who is training his retailers across 1 lakh retail touch points to spread awareness about the benefits of transacting online. “The biggest impediment is fear, and removing it from the minds would be a big blow to cash,” he says. A bit of hand-holding, he lets on, would make a world of difference. The way Dhabhai sees it, cash and cashless can complement each other for the time being; in the long run, cash won’t be dead but it may well be cashless that’s king.\n<\/p><\/body>","next_sibling":[{"msid":55645867,"title":"PM Modi launches Indian Police app that helps you locate nearest police stations","entity_type":"ARTICLE","link":"\/news\/pm-modi-launches-indian-police-app-that-helps-you-locate-nearest-police-stations\/55645867","category_name":null,"category_name_seo":"telecomnews"}],"related_content":[],"msid":55646009,"entity_type":"ARTICLE","title":"Demonetisation: How digital challenges turn into opportunities like mobile wallet in rural India","synopsis":"Home to about 870 million people, the countryside will be in the thick of action for the rest of the decade, according to a recent BCG report.","titleseo":"telecomnews\/demonetisation-how-digital-challenges-turn-into-opportunities-like-mobile-wallet-in-rural-india","status":"ACTIVE","authors":[{"author_name":"Rajiv Singh","author_link":"\/author\/479211175\/rajiv-singh","author_image":"https:\/\/etimg.etb2bimg.com\/authorthumb\/479211175.cms?width=100&height=100&hid=268","author_additional":{"thumbsize":false,"msid":479211175,"author_name":"Rajiv Singh","author_seo_name":"rajiv-singh","designation":"Editor","agency":false}}],"Alttitle":{"minfo":""},"artag":"ET Bureau","artdate":"2016-11-27 10:17:08","lastupd":"2016-11-28 14:58:00","breadcrumbTags":["demonetisation","Mobile wallet","ItzCash","PayTM","Freecharge","Payworld","StoreKing"],"secinfo":{"seolocation":"telecomnews\/demonetisation-how-digital-challenges-turn-into-opportunities-like-mobile-wallet-in-rural-india"}}" data-authors="[" rajiv singh"]" data-category-name="" data-category_id="" data-date="2016-11-27" data-index="article_1">

![]()

但与其他印度村庄,Dhaturi可能在一个非凡的变换后政府的激进demonetisation11月8日。过渡到数字化的生活方式已经开始,和苏雷什朋友在这种变化的先锋。在他的小照相馆,Pal双打作为一个零售商Payworld电子事务处理平台,帮助人们打开一个辅助手机钱包帐户。“即使那些没有智能手机可以使用钱包,”他说。

村里的登录

Payworld,超过1亿个用户和1多数零售接触点,涉及印度630个城市和80000个村庄到11月的第一个星期,在新用户增长了25%——主要来自农村和城乡交界地区,在过去的两个星期。“我们不能实现在过去九年被纳兰德拉·莫迪,促进立刻“Payworld首席运营官Praveen Dhabhai脱口而出。“超过93%的印度农村人没有任何数字交易完成。所以真正的潜在的谎言。”

Dhabhai不是唯一一个冲在一个机会采取数字现金支付给农村消费者demonetisation。ItzCash电子支付公司成立于2006年,也是关注更大份额的农村的钱包。虽然大多数球员,包括中国电子商务主要Alibaba-backedPaytm和Snapdeal-ownedFreeCharge迎合印度的前10%,ItzCash计划保持专注于巴拉特大约66%的国家居住,ItzCash Naveen苏亚的常务董事说。omni-channel存在的公司,通过媒体,移动钱包和卡,存在3000个城镇和城市,声称已经自11月8日交易量激增了40%。“在未来几个季度,我们的大部分增长将推动巴拉特,”他说。

印度农村、巴拉特的确看起来像一个土地市场的黄金机会,包括移动钱包的球员。原因:大约有8.7亿人,农村的厚的行动将在剩下的十年中,根据管理咨询公司波士顿咨询公司最近的一份报告。题为“上升连接消费者在印度农村”,波士顿咨询公司预测,农村用户将占大约一半的印度互联网用户在2020年。而连接农村消费者的数量预计将从1.2亿年的2015增加到近3.15亿在2020年一年复合增长率将近30%——农村增长将大大超过在城市中心。和推动农村的增长,增加了该报告发表在8月,便宜手机,无线数据网络传播和消费者行为的发展。

Demonetisation后

现在,有demonetisation效果。帕可拉Sohan Ram,路边小贩出售面包,面条和茶从他小临时店在哈里亚纳邦Kurar村,是一个无现金的未来做准备。他说,尽管价格最高的产品销售是Rs 50下,移动钱包确保用户支付每一个卢比,通常很多人跳过援引缺少零钱。“现在的手机钱包不能找借口,”他笑着说。

仅一箭之遥拉从Ram的摊位是一个商店。基肖尔集,经营者,犹豫后最初几天禁止流通。他认为政府可能回滚和现金将仍然继续支付的主要媒介。但是当商业枯竭,人们跑出现金,52岁的集快速cardswiping机器安装和下载MobiKwik,在线支付系统。“迟到总比不到好,”他说。尽管他面临初期问题在理解技术的头两天,他现在舒服地进行交易。

用户像Ram和集给希望移动钱包产业,预计将从154卢比在2016财政年度到2022年的30000卢比。这意味着一个相应的跳的移动钱包事务:从20600卢比到55个十万的卢比在同一时期,根据最近的一项研究Assocham-RNCOS题为“印度M-wallet市场:预计2022年。”

“从当地周期店主一个卖甘蔗汁神庙祭司,都开始使用手机钱包,“认为Bipin普里特辛格MobiKwik的创始人。

成立于2009年,MobiKwik声称有超过4000万个用户,一个商人的超过2.5十万的网络。该公司成立于2009年,见过最惊人的增长的用户群后,11月8日:超过500万在短短两周。

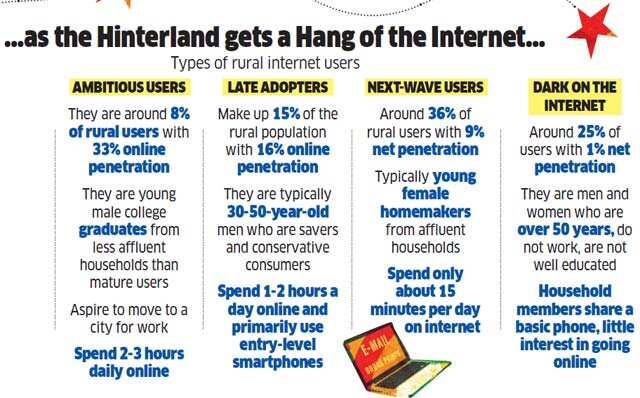

“demonetisation之前,钱包是一个选项。现在他们需要,”辛格说,他的公司正在增加其地勤人员强度从1000年到12000年就读当地的商人钱包支付。但是辛格还打算做些什么——他声称是改变,接触下一波互联网用户在印度农村:年轻的家庭主妇,那些已经在线但花几分钟上网,占36%以上的农村网民。“如果集团的规模是巨大的,潜力是巨大的,”辛格说。

这种增长潜力不能想当然,。仅几公里Dhaturi,邻村的Lalheri Khurd,生活Rampal独角鲸,一位55岁的农场工作者来说,现金一直是国王。他没有心情处理数字,尽管拥有摩托罗拉智能手机3 g连接。原因:技术和未知的恐惧。

“我的钱可以消失。最好让它在家里,”他说。那么为什么他有一个智能手机,如果他只是想用它来打电话?“问我的儿子。他买了它,”快照独角鲸,他反过来是他十几岁的孙子Sohan打断了。“我的父亲有一个Facebook账户但是互联网不能正常工作,”他说,补充说,电话没有任何其他应用程序,甚至Paytm。“我在电视上看过它的广告”,他笑了。

独角鲸是困惑的人们争相使用手机钱包和借记卡。问他关于生活demonetisation之后,老人给一个明确的答复:“我仍在使用现金,总是使用现金。“让独角鲸公司Umesh中间人,相邻的另一个农场工作者Ramnagar村庄。Dalal最大的观点坚持旧的生活方式的心态:“我为什么要去无现金吗?它将如何改变我的生活?”旁边一个巨大的Jio招牌,Dalal检查WhatsApp Micromax画布移动消息。“有很多优点在只在现金交易,”他说。

无现金牛

随着印度需要一步构建一个无现金的经济,它变得明显,最大的挑战莫迪的设想为一个无现金的国家将来自巴拉特,由于不稳定的网络连接,可怜的智能手机普及率- 30%,说当地网络——加上铁杆的习惯依赖现金交易。

专家认为,印度政府轻率的推动无现金可能太多,太快。而主要目标应该是确保每个人都有一个银行账户,和所有银行应该使它容易交易数字,现实情况是,许多小型银行不提供数字银行,说杰西保罗,保罗作家的创始人营销咨询公司。手机钱包而言,她所指出的那样,有三个主要问题。首先是成本。有一个费用转账到钱包,然后从钱包的商人。第二个问题是信任。害怕欺诈高对于任何数字工具。和可靠性;网络玩家可以确保会有100%正常运行时间的网络?

复合重要的是另一个问题:当一个人不消费为冲动购物经常因为缺乏资金,现有的付款方式,现金,变得更加方便。“目前没有理由一个人放弃现金和最终支付额外的交易费用花hardearned钱,”保罗说。

没有人理解的力量的现金比bloom Gundaiah,创始人StoreKing协助电子商务平台。可能仍有一段时间印度是准备做一个大塑料交易资金的一部分,和demonetisation似乎忽略,他认为。

“现金的美妙之处在于,它只是作品,“Gundaiah说,谁是一个独特的商业模式允许人们购买使用现金,尽管使用电子商务。附近零售商,手持平板电脑和互联网连接,帮助客户选择产品从StoreKing的网上购物平台,和现金付款。

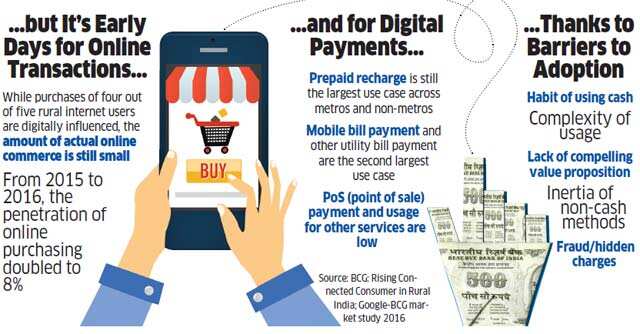

问他为什么人们在印度农村不是网上购物,和Gundaiah列表一堆刺激物:每个村庄没有销代码,这使得交货困难,文化水平低,英语语言障碍和缺乏信任的网络。“超过85%的人口没有使用借记卡和信用卡,一半的人口无法达到传统快递服务,”他说。所以,尽管金钱和意图,在小城镇和村庄的人们无法网上购物。

即使在农村地区的人们使用移动互联网,这并不意味着他们在网上交易的一种情绪。Gundaiah说,在农村用户,访问网络娱乐的主要原因,其次是沟通和社交网络。“我们有了农村人口与辅助商业,”他说,并补充说他希望在未来几年内达到5亿人。“没有办法Flipkart公司或亚马逊可以达到内部像。”

零售分析师认为,数字化印度农村的任务可能是具有挑战性的,但并非不可能。萨洛尼•Nangia零售咨询公司Technopak Advisors的总裁说,对于大多数农村印度人来说,银行和网络都是一个新的体验。所以他们害怕都是很自然的。“有一个巨大的未知的恐惧,尤其是当它涉及到钱,”她说。

虽然承认会有故障在转型,Nangia认为首先必须在某个地方。她指出,最初怀疑周围Aadhaar当它在2009年推出。但在七年内的独特身份项目录取10.7亿人,全国人口的88%左右。“应该关注教育和传播意识,”她说。

手机钱包的球员,对他们来说,已经在工作了。带头的喜欢Praveen Dhabhai Payworld,训练他零售商在多数零售接触点传播对网上交易的好处。“最大的障碍是恐惧,和删除它从心中对现金将是一个很大的打击,”他说。牵手,他让,将使一个不同的世界。Dhabhai看来,现金和无现金可以暂时互补;从长远来看,现金不会死,但它很可能是无现金的国王。

Dhaturi, a dusty village in Haryana some 54 kilometres from the national capital, is like any other hamlet in North India: a cluster of half-plastered, concrete buildings housing kirana stores; semi-paved streets, on which buffaloes saunter, flanked by thatched huts; a sleepy market; and huge swathes of agricultural fields that bear black marks of recently burnt stubble.

\n

But unlike many other Indian villages, Dhaturi may be in the midst of a remarkable transformation after the government’s radical demonetisation<\/a> drive on November 8. A transition to a digital way of life has begun, and Suresh Pal is at the vanguard of this change. In his small photo studio, Pal doubles up as a retailer for Payworld<\/a>, an electronic transaction processing platform, helping people open an assisted mobile wallet<\/a> account. “Even those without smartphones can use the wallet,” he says.

\n

\nThe Village Logs In <\/strong>

\nPayworld, which had over 100 million users and 1 lakh retail touch points across 630 cities and 80,000 villages till the first week of November, has seen a 25% jump in new users — mostly from rural and semi-urban areas — over the last two weeks. “What we couldn’t achieve during the last nine years was facilitated instantly by Narendra Modi,” gushes Payworld chief operating officer Praveen Dhabhai. “Over 93% of people in rural India have not done any digital transactions. So the real potential lies there.”

\n

\n\n\t\n\t

\n

\n\n\t\n\t

\n

Dhabhai is not the only one rushing in to cash in on an opportunity to take digital payments to rural consumers post demonetisation. ItzCash<\/a>, a digital payments company founded in 2006, too is eyeing a larger share of the rural wallet. While most players, including Chinese ecommerce major Alibaba-backed Paytm<\/a> and Snapdeal-owned FreeCharge<\/a>, are catering to the top 10% of India, ItzCash plans to keep its focus on Bharat where roughly 66% of the country resides, says managing director of ItzCash Naveen Surya. The company, with an omni-channel presence through outlets, mobile wallets and cards, is present across 3,000 towns and cities, and claims to have seen a 40% spike in transaction volumes since November 8. “Over the next few quarters, most of our growth would be fuelled by Bharat,” he says.

\n

\n\n\t\n\t

\n

\nRural India, or Bharat, indeed looks like a land of golden opportunity for marketers, including mobile wallet players. Reason: home to about 870 million people, the countryside will be in the thick of action for the rest of the decade, according to a recent report by management consultancy firm BCG. Titled “Rising Connected Consumer in Rural India”, BCG predicts that rural users will constitute about half of all Indian internet users in 2020. While the number of connected rural consumers is expected to increase from about 120 million in 2015 to almost 315 million in 2020 — a compounded growth of almost 30% a year — rural growth will significantly outpace growth in urban centres. And what’s driving the rural growth, adds the report that was published in August, are cheaper mobile handsets, spread of wireless data networks and evolving consumer behaviour.

\n

\n\n\t\n\t

\n

\nAfter Demonetisation <\/strong>

\nNow, there’s the demonetisation effect. Sohan Ram, a roadside vendor selling bread pakoras, noodles and tea from his small makeshift shop at Kurar village in Haryana, is getting ready for a cashless future. He says that although the highest priced product he sells is under Rs 50, mobile wallets ensure that users pay up every rupee, which many of them usually skipped citing paucity of loose change. “Now the ones with mobile wallets can’t make an excuse,” he grins.

\n

\n\n\t\n\t

\n

\nJust a stone’s throw from Ram’s stall is a kirana store. Kishore Chand, the proprietor, dithered for the first few days after demonetization. He thought the government might roll back the move and cash would still continue to be the main medium of payment. But when business dried up as people ran out of cash, 52-year-old Chand quickly installed a cardswiping machine and downloaded MobiKwik, an online payment system. “It’s better late than never,” he says. Although he faced teething problems in the first two days in understanding the technology, he’s now comfortably making transactions.

\n

\n\n\t\n\t

\n

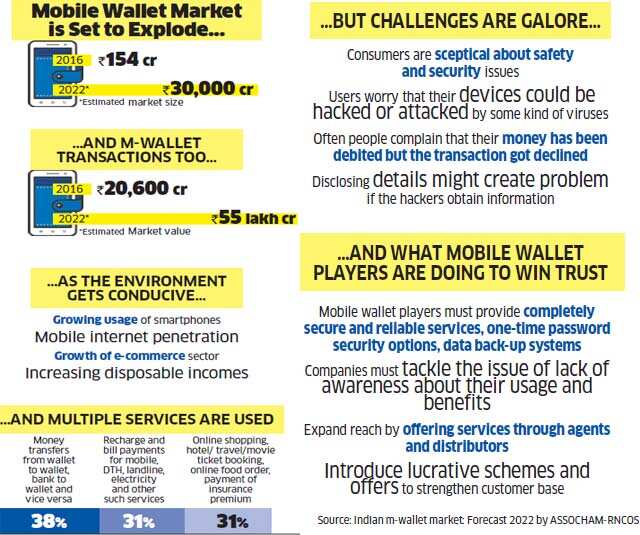

\nIt’s users like Ram and Chand who give hope to the mobile wallet industry, which is projected to jump from Rs 154 crore in fiscal year 2016 to Rs 30,000 crore by 2022. This means a corresponding jump in the value of mobile wallet transactions: from Rs 20,600 crore to Rs 55 lakh crore during the same period, according to a recent study by Assocham-RNCOS titled “Indian M-wallet Market: Forecast 2022.”

\n

\n“From a local cycle shop owner to a sugarcane juice seller to even a temple priest, all have started using mobile wallets,” contends Bipin Preet Singh, cofounder of MobiKwik.

\n

\n\n\t\n\t

\n

\nFounded in 2009, MobiKwik claims to have over 40 million users, and a merchant network of over 2.5 lakh. The company, which was founded in 2009, has seen the most astonishing growth in its user base after November 8: over 5 million in just two weeks.

\n

\n\n\t\n\t

\n

\n“Before demonetisation, wallets were an option. Now they are a need,” says Singh, whose company is increasing its ground staff strength from 1,000 to 12,000 to enrol local merchants for wallet payments. But what Singh also plans to do — and he claims to be a game-changer — is reach out to the next wave of internet users in rural India: young homemakers, who are already online but spend a few minutes surfing the net, constitute over 36% of rural internet users. “If the size of the group is massive, the potential it has is gigantic,” says Singh.

\n

\n\n\t\n\t

\n

\nSuch growth potential can’t be taken for granted, though. Just a few kilometres from Dhaturi, in the neighbouring village of Lalheri Khurd, lives Rampal Narwal, a 55-year-old agriculturist for whom cash has always been king. And he’s in no mood to transact digitally, despite boasting a Motorola smartphone with a 3G connection. Reason: the fear of technology and the unknown.

\n

\n\n\t\n\t

\n

\n“My money can vanish. It’s best to keep it at home,” he says. Why then does he have a smartphone if he just wants to use it to make calls? “Ask my son. He bought it,” snaps Narwal, who in turn is interrupted by his teenaged grandson Sohan. “My father has a Facebook account but the internet doesn’t work properly,” he says, adding that the phone doesn’t have any other app. Not even Paytm. “I have seen its advertisement on TV,” he smiles.

\n

\nNarwal is bemused to see people scrambling to use mobile wallets and debit cards. Ask him about life after demonetisation, and the old man gives a clear-cut reply: “I still use cash, and will always use cash.” Keeping Narwal company is Umesh Dalal, another agriculturist in the adjoining Ramnagar village. Dalal’s biggest argument in persisting with the old way of life is mindset: “Why should I go cashless? How will it change my life?” Sitting next to a huge Jio signboard, Dalal checks his WhatsApp messages on his Micromax Canvas mobile. “There is much merit in transacting only in cash,” he says.

\n

\n\n\t\n\t

\n

\nThe Cashless Cow <\/strong>

\nAs India takes a step towards building a cashless economy, it’s becoming clear that the biggest challenge to Narendra Modi’s vision for a cashless country will come from Bharat, thanks to erratic internet connectivity, poor smartphone penetration — 30%, says CyberMedia Research — coupled with die-hard habits of relying on cash for transactions.

\n

\nExperts contend that the government’s headlong push for a cashless India may be too much, too soon. While the primary goal should be to ensure that everyone has a bank account, and all banks should make it easy to transact digitally, the reality is that many smaller banks do not offer digital banking, says Jessie Paul, founder of Paul Writer, a marketing advisory firm. As far as mobile wallets are concerned, she points out, there are three major issues. First is cost. There is a fee to transfer money to the wallet, and then from wallet to merchant. The second issue is trust. Fear of fraud is high for any digital tool. And there’s reliability; can internet players ensure that there will be 100% uptime of the network?

\n

\nCompounding matters is another problem: when a person doesn’t consume frequently because of paucity of money for impulse purchases, the existing mode of payment, cash, becomes more convenient. “Currently there is no reason for a person to abandon cash and end up paying additional transaction fees to spend their hardearned money,” says Paul.

\n

Nobody understands the power of cash better than Sridhar Gundaiah, founder of StoreKing<\/a>, an assisted ecommerce platform. There may still be some time before India is ready to do a large part of its transactions in plastic money, and demonetisation seems to ignore that, he reckons.

\n

\n“The beauty of cash is that it just works,” says Gundaiah, who follows a unique business model of allowing people to purchase using cash, albeit using ecommerce. The neighbourhood retailer, armed with a tablet and an internet connection, assists customers choose products from StoreKing’s online shopping platform, and the payment is made in cash.

\n

\nAsk him why people in rural India are not shopping online, and Gundaiah lists out a bunch of irritants: every village does not have a pin code, which makes deliveries difficult, low literacy levels, English language barrier and lack of trust in the internet. “Over 85% of the population has no access to debit and credit cards and half of the population is not reachable by traditional courier services,” he says. So, despite having the money and the intent, people in small towns and villages are unable to shop online.

\n

\n\n\t\n\t

\n

\nAnd even if people in rural areas are using mobile internet, it doesn’t mean they are in a mood to transact online. Gundaiah says that among rural users, the primary reason for accessing the net is entertainment, followed by communication and social networking. “We have tapped the rural population with assisted commerce,” he says, adding that he hopes to reach 500 million people in the next couple of years. “There is no way a Flipkart or an Amazon can reach the interiors like we can.”

\n

\nRetail analysts maintain that the task to digitise rural India might be challenging, but not impossible. Saloni Nangia, president of retail consultancy firm Technopak Advisors, says for a large majority of rural Indians, both banking and internet are a new experience. So it’s natural for them to fear both. “There is a huge fear of the unknown, especially when it comes to money,” she says.

\n

\nWhile conceding that there would be hitches in making the transition, Nangia believes that a start has to be made somewhere. She points to the initial scepticism around Aadhaar when it was introduced way back in 2009. But within seven years the unique identity project has enrolled 1.07 billion people, or about 88% of the country’s population. “The focus should be on educating and spreading awareness,” she says.

\n

\nMobile wallet players, for their part, are already on the job. Taking the lead are the likes of Praveen Dhabhai of Payworld, who is training his retailers across 1 lakh retail touch points to spread awareness about the benefits of transacting online. “The biggest impediment is fear, and removing it from the minds would be a big blow to cash,” he says. A bit of hand-holding, he lets on, would make a world of difference. The way Dhabhai sees it, cash and cashless can complement each other for the time being; in the long run, cash won’t be dead but it may well be cashless that’s king.\n<\/p><\/body>","next_sibling":[{"msid":55645867,"title":"PM Modi launches Indian Police app that helps you locate nearest police stations","entity_type":"ARTICLE","link":"\/news\/pm-modi-launches-indian-police-app-that-helps-you-locate-nearest-police-stations\/55645867","category_name":null,"category_name_seo":"telecomnews"}],"related_content":[],"msid":55646009,"entity_type":"ARTICLE","title":"Demonetisation: How digital challenges turn into opportunities like mobile wallet in rural India","synopsis":"Home to about 870 million people, the countryside will be in the thick of action for the rest of the decade, according to a recent BCG report.","titleseo":"telecomnews\/demonetisation-how-digital-challenges-turn-into-opportunities-like-mobile-wallet-in-rural-india","status":"ACTIVE","authors":[{"author_name":"Rajiv Singh","author_link":"\/author\/479211175\/rajiv-singh","author_image":"https:\/\/etimg.etb2bimg.com\/authorthumb\/479211175.cms?width=100&height=100&hid=268","author_additional":{"thumbsize":false,"msid":479211175,"author_name":"Rajiv Singh","author_seo_name":"rajiv-singh","designation":"Editor","agency":false}}],"Alttitle":{"minfo":""},"artag":"ET Bureau","artdate":"2016-11-27 10:17:08","lastupd":"2016-11-28 14:58:00","breadcrumbTags":["demonetisation","Mobile wallet","ItzCash","PayTM","Freecharge","Payworld","StoreKing"],"secinfo":{"seolocation":"telecomnews\/demonetisation-how-digital-challenges-turn-into-opportunities-like-mobile-wallet-in-rural-india"}}" data-news_link="//www.iser-br.com/news/demonetisation-how-digital-challenges-turn-into-opportunities-like-mobile-wallet-in-rural-india/55646009">

评论

现在评论 阅读评论(1)所有评论

找到这个评论进攻?

下面选择你的理由并单击submit按钮。这将提醒我们的版主采取行动