独家

政府不放宽规则Tata-DoCoMo纠纷

政府认为,没有理由放松在规则允许DoCoMo退出电信合资企业以预先确定的价格和再见

政府认为,没有理由放松在规则允许DoCoMo退出电信合资企业以预先确定的价格和再见

新德里:政府认为没有理由规则允许的任何放松DoCoMo退出其电信合资企业以预先确定的价格和再见。

新德里:政府认为没有理由规则允许的任何放松DoCoMo退出其电信合资企业以预先确定的价格和再见。 消息人士说,干预Tata-DoCoMo情况将导致回顾修正案的规定,这对一个公司不能做。还有其他几个例类似的问题。在任何情况下,政府反对任何回顾行动。

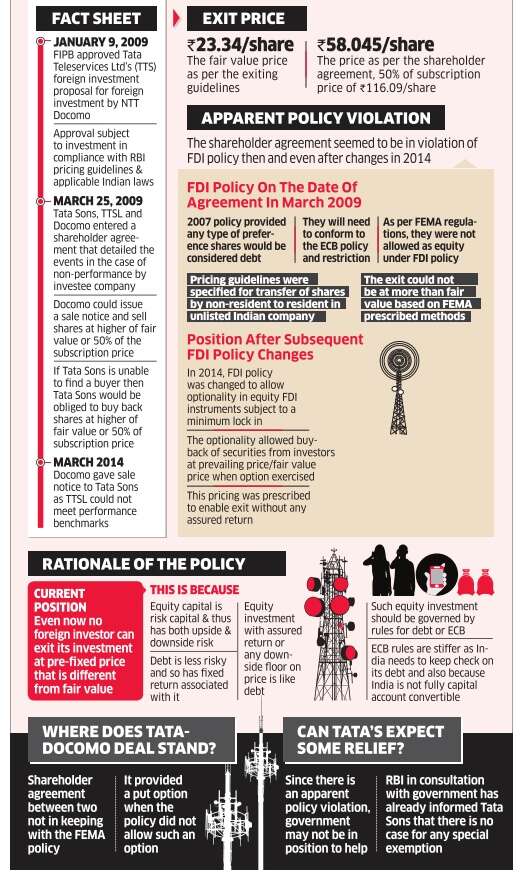

消息人士说,干预Tata-DoCoMo情况将导致回顾修正案的规定,这对一个公司不能做。还有其他几个例类似的问题。在任何情况下,政府反对任何回顾行动。 NEW DELHI: The government is of the view that there is no case for any relaxation in rules to allow DoCoMo<\/a> to exit its telecom joint venture with the Tatas at a pre-determined price. Sources said that intervening in the Tata-DoCoMo case would result in retrospective amendment of rules, which can\u2019t be done for one company. There are several other cases with similar issues. And in any case, the government is averse to any retrospective action.

NEW DELHI: The government is of the view that there is no case for any relaxation in rules to allow DoCoMo<\/a> to exit its telecom joint venture with the Tatas at a pre-determined price. Sources said that intervening in the Tata-DoCoMo case would result in retrospective amendment of rules, which can\u2019t be done for one company. There are several other cases with similar issues. And in any case, the government is averse to any retrospective action.

解决post-Budget记者会在孟买,投资和公共资产管理部门(Dipam)部长Tuhin Kanta Pandey说,他的部门将持有该股。这将是类似于ITC和其他政府的控股公司,收购由于泌尿道感染救助。