MUMBAI: In what could be an industry first, promoters of telecom tower company GTL Infrastructure have recommended that its lenders convert debt to take majority shares to reduce the complexity of its borrowing and secure a suitor, said two people familiar with the details.

MUMBAI: In what could be an industry first, promoters of telecom tower company GTL Infrastructure have recommended that its lenders convert debt to take majority shares to reduce the complexity of its borrowing and secure a suitor, said two people familiar with the details.\n

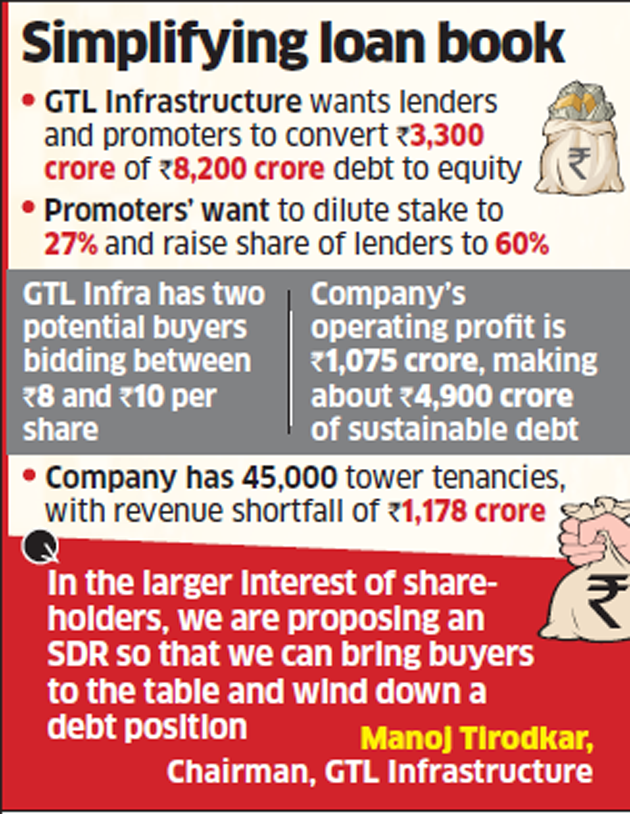

\nThe company’s board on Monday approved such a move that is likely to be presented to investors over the course of this week. The move involves lenders and promoters converting Rs 3,300 crore of their Rs 8,200 crore debt to shares at par value, or Rs 10 per share, in GTL Infrastructure. This would give lenders 60 per cent in the company and dilute promoters’ stake to 27 per cent.

\n

\nAn E&Y report made for investors of GTL Infrastructure puts its operating profit at Rs 1,075 crore, making about Rs 4,900 crore of sustainable debt under strategic debt restructuring (SDR) norms that has put power in the hands of lenders to seize assets of companies that are unable to repay loans.

\n

\"In the larger interest of shareholders, we are proposing an SDR so that we can bring buyers to the table and wind down a debt position that has been hovering over lenders and promoters alike for the last five years,\" said Manoj Tirodkar<\/a>, chairman of GTL Infrastructure.

\n

\nInvestors demand a simplified loan book before they make an offer, although there are some willing bidders, he said.

\n

\nA banker familiar with the matter said GTL Infrastructure has two potential buyers bidding between Rs 8 and Rs 10 per share with a guaranteed 80 per cent in the company with no legally questionable debt.

\n

\nHe said the SDR process would take around a year to complete. \"By then, operating profit should grow by nearly 40 per cent given the turnaround in the telecom tower company in the last six months.\"

\n

\n

\n

\n

\nWith that, the company, at a similar valuation to deals this year, would fetch around Rs 11 per share and would mean no haircuts for lenders, he added.

\n

GTL Infrastructure, along with its subsidiary Chennai Network Infrastructure<\/a>, which was acquired from Aircel<\/a> in 2010 for Rs 8,062 crore, has around 45,000 telecom towers with a tenancy ratio of 1.86, comparable with that of Viom Networks<\/a>’ 2.1 ratio at the time of acquisition.

\n

\n\"It is surprising but they (GTL Infrastructure) are getting more Reliance Jio tenancies than some of the bigger competitors, but it will really improve cash flows,\" said an analyst with an MNC brokerage.

\n

\nThis year has indeed been big for the telecom industry. American Tower Corp acquired Tata-owned Viom Networks for Rs 21,000 crore. Reliance Jio has been leasing towers aggressively across operators and in August gave contracts for around 24,000 towers. GTL Infrastructure too has secured around 6,000 of those tenancies.

\n

\nWhile the object of the SDR scheme was for lenders to acquire and sell the asset to a strategic company, it is yet to be seen in action.

\n

\nEarlier this year, after lenders of Amtek Auto effected such an acquisition, actual divestment has been held up with the company’s worth reducing continuously. The GTL Infrastructure deal, if approved, will be a trend-setter as was its corporate debt restructuring in 2011.

\n

\nWhat happened five years ago<\/strong>

\nIn 2009-10, the telecom tower sector expected an unparalleled explosion since licences had been given to five players who would supposedly role out networks. Simultaneously, telecom operators were looking to raise funds to brace for a price battle that new players would likely initiate.

\n

\nAs part of that, Aircel sought to sell its 17,000 towers and found a buyer in GTL Infrastructure at a whopping Rs 8,062 crore. However, by the end of 2010, it became clear that there was a scam in awarding the five licences and in February 2012, these licenses were revoked, scuttling all growth plans to tower companies.

\n

\nAircel’s acquisition also included GTL Infrastructure’s first right to provide around 60,000 more tenancies that the operator was to add over the next two years. Not only did the new comers back out of commitments, so did Aircel.

\n

\nBy 2011, GTL Infrastructure, along with two group companies, underwent corporate debt restructuring, in which lenders took a haircut, but created a plan to keep the company running. However, in 2012 when licences were irrevocably cancelled, even these plans came undone.

\n

\nThe group has repaid around Rs 6,000 crore in debt and interest over the last five years, but the company cash flow is insufficient to service the outstanding loans.

\n

\nAn earlier estimate pegged GTL Infrastructure to have 70,300 tenancies by December 2015. Instead, the company has merely 45,000 now. From these, the company estimates a revenue shortfall of Rs 1,178 crore.

\n

\nSince a telecom tower company makes the expense to set up the tower up front, most of the rentals from new tenancies translate directly to operating profit.

\n

\nTypically, around 60 per cent of the revenue from the second tenancy on a tower flows to profit. Therefore a revenue shortfall directly affects the company’s ability to repay loans.\n\n<\/body>","next_sibling":[{"msid":54418527,"title":"Telcos shouldn't oppose ombudsman for consumer disputes, say Trai officials","entity_type":"ARTICLE","link":"\/news\/telcos-shouldnt-oppose-ombudsman-for-consumer-disputes-say-trai-officials\/54418527","category_name":null,"category_name_seo":"telecomnews"}],"related_content":[],"msid":54418649,"entity_type":"ARTICLE","title":"GTL Infrastructure promoters want lenders to convert debt to take majority stake","synopsis":"Telecom tower company seeks Rs 3,300 crore of debt to be converted into equity giving lenders around 60 per cent stake in the company.","titleseo":"telecomnews\/gtl-infrastructure-promoters-want-lenders-to-convert-debt-to-take-majority-stake","status":"ACTIVE","authors":[{"author_name":"Deepali Gupta","author_link":"\/author\/479212148\/deepali-gupta","author_image":"https:\/\/etimg.etb2bimg.com\/authorthumb\/479212148.cms?width=100&height=100&hostid=268","author_additional":{"thumbsize":false,"msid":479212148,"author_name":"Deepali Gupta","author_seo_name":"deepali-gupta","designation":"Correspondent","agency":false}}],"Alttitle":{"minfo":""},"artag":"ET Bureau","artdate":"2016-09-20 08:23:02","lastupd":"2016-09-20 08:25:54","breadcrumbTags":["Aircel","Manoj Tirodkar","Telecom equipment","Viom Networks","Chennai Network Infrastructure"],"secinfo":{"seolocation":"telecomnews\/gtl-infrastructure-promoters-want-lenders-to-convert-debt-to-take-majority-stake"}}" data-authors="[" deepali gupta"]" data-category-name="" data-category_id="" data-date="2016-09-20" data-index="article_1">

孟买:这可能是一个行业第一,电信塔公司的发起人GTL基础设施建议其银行债务转换为采取多数股票减少借贷和安全的一个追求者的复杂性,说两位知情人士透露细节。

孟买:这可能是一个行业第一,电信塔公司的发起人GTL基础设施建议其银行债务转换为采取多数股票减少借贷和安全的一个追求者的复杂性,说两位知情人士透露细节。公司董事会周一批准了这一举动,很可能是在本周的形式提供给投资者。此举涉及银行和推动者转换3300卢比8200卢比的债务与股票面值,或每股10卢比GTL基础设施。这将使银行公司和稀释发起人的股份的60%到27%。

安永报告为投资者GTL的基础设施使其营业利润在1075卢比,使大约4900卢比的可持续战略下债务债务重组(SDR)规范,把权力交给了银行抓住资产的公司无法偿还贷款。

“股东更大的利益,我们提出一个特别提款权,这样我们可以降低买家表和风力已经悬停在贷款人的债务状况,启动子一样,过去的五年里,”说Manoj Tirodkar董事长GTL基础设施。

投资者要求简化贷款在出价之前,虽然有一些愿意买家,他说。

银行家知情人士说GTL基础设施之间有两个潜在买家竞标Rs每股8和10卢比公司保证80%没有合法的问题债务。

他说,特别提款权过程需要一年左右才能完成。“到那时,营业利润将增长近40%,鉴于好转电信塔公司在过去的六个月。”

,该公司在今年类似的估值交易,将获取Rs每股11和银行也就意味着将没有理发,他补充说。

GTL基础设施,连同它的子公司钦奈网络基础设施,从收购Aircel2010年为8062卢比,大约有45000电信大楼租赁比率为1.86,可比的Viom网络2.1比当时的收购。

“很惊讶但是他们基础设施(GTL)越来越依赖Jio占有权比一些更大的竞争对手,但它真的会改善现金流,“跨国公司的分析师说。

今年确实大的电信行业。美国塔集团收购Tata-owned Viom网络为21000卢比。依赖Jio已经租赁塔积极跨运营商和8月给合同约24000塔。GTL那些佃户的基础设施也已获得约6000。

尽管SDR计划的对象是银行收购和出售资产战略的公司,仍有待观察。

今年早些时候,贷款人Amtek汽车影响这样的收购后,实际撤资举行了该公司的价值不断降低。GTL基础设施交易,如果得到批准,将领导新潮的人,于2011年其企业债务重组。

五年前发生了什么

在2009年10月,电信塔部门预期一个无与伦比的爆炸以来牌照已经给那些我们以为会作用的五名球员离开网络。同时,电信运营商想要筹集资金做好价格战争,新玩家可能会启动。

作为其中的一部分,Aircel试图出售其17000年塔,发现一个买家在GTL基础设施在高达8062卢比。然而,到2010年底,很明显,有一个骗局授予五个牌照和2012年2月,这些许可证被撤销,所有塔公司发展计划告吹。

Aircel收购还包括GTL基础设施的第一个提供约60000更占有权,操作员被添加在未来两年。不仅新来者的承诺,Aircel也是如此。

GTL基础设施,到2011年,两家集团公司,经历了企业债务重组,银行把理发,但创建了一个计划,以使公司运行。然而,2012年执照不可逆转地取消时,即使这些计划还没有制定出来。

集团偿还约6000卢比的债务和利息在过去五年,但该公司现金流不足以未偿还贷款服务。

早些时候估计挂钩GTL基础设施租赁70300在2015年12月。相反,该公司仅仅是现在的45000。从这些,该公司估计1178卢比的收入不足。

由于电信塔公司制造费用设置塔,大部分的租金从营业利润的新租户直接转换。

一般来说,约60%的收入来自第二租赁塔流的利润。因此收入不足直接影响该公司偿还贷款的能力。

评论

现在评论 阅读评论(1)所有评论

找到这个评论进攻?

下面选择你的理由并单击submit按钮。这将提醒我们的版主采取行动