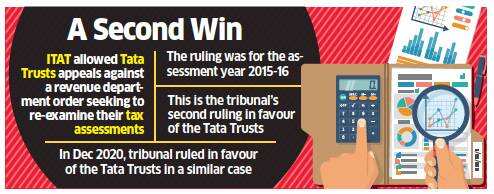

Mumbai: The Income Tax Appellate Tribunal has upheld the tax-exempt status of the Tata Trusts<\/a> and allowed their appeals against a revenue department order seeking to re-examine their tax assessments. 孟买:所得税上诉法庭维持的免税地位塔塔信托并允许他们上诉寻求重新审视其税收收入部门评估。

The Mumbai bench of the ITAT rejected the income tax department’s claims that the trusts had violated laws related to charitable trusts by holding shares of Tata Sons<\/a>.

This is the tribunal’s second ruling in favour of the Tata Trusts – Sir Ratan Tata Trust<\/a>, Sir Dorabji Tata Trust and the JRD Tata Trust. The ruling was for the assessment year 2015-16. In December 2020, the tribunal ruled in favour of the Tata Trusts in an identical case for assessment year 2014-15.

“Since the revision order under Section 263 of the Act for the assessment year 2015-16 was passed on identical facts and circumstances prevailing for the year 2014-15 in all the three trusts... all the three appeals... shall apply mutatis mutandis to this assessment year also,” a two-member bench of the ITAT said in its order of March 8, which was made available on Monday. “The operative portion of the said order of the tribunal is not reproduced herein for the sake of brevity. Accordingly, the grounds raised by the assessee are allowed.”

In its December 2020 order, the tribunal observed that “as long as the shares are part of the corpus, as on June 1, 1973, or the shares are received as an accretion to the shares being held to be part of the corpus, the provisions of Section 13(1)(c) will not come into play.”

The order was a win for Tata Trusts in its battle to retain tax-exempt status. The tribunal’s observations on share ownership are likely to influence a case where the trusts challenged the tax department’s cancellation of their registrations.

In 2016, the commissioner of income tax (exemption) (CIT-E) had threatened to upend the decades-old ownership of Tata Sons by the trusts by alleging that such shareholdings violated income tax laws.

As per the December 2020 ruling, the genesis of the dispute lay in the 2016 order by the CIT-E, which rejected the grant of tax exemption to Sir Ratan Tata Trust, Sir Dorabji Trust and the JRD Tata Trust by the assessing officer, calling it erroneous and prejudicial to the interests of revenue and requiring revision. The matter pertained to the returns filed for AY14-15 (financial year 2013-14) by Sir Dorabji Tata Trust.

The Tata Trusts appealed to the tribunal, denying the claims of the CIT-E.

The Trusts denied that they had violated income tax laws by indulging in “prohibited modes of investment” – that is, ownership of Tata Sons shares. They pointed out that tax exemption had been granted in previous years and that all the shares held in FY13-14 were held by the trusts before June 1, 1973, and subsequent additions to the corpus were only through bonus shares. It further stated that all the shares were held by them as corpus and the dividend income from these shares was used by the Tata Trusts for its charitable objects.

According to Ashish K Singh, managing partner of law firm Capstone Legal, each assessment year is required to be considered separately.

“The reasoning given by ITAT is that since the revision order which was challenged has been decided in favour of Tata Trusts for the assessment year in 2014-15, similar order is required to be passed for the subsequent year as well as the facts are identical,” said Singh.

<\/p><\/body>","next_sibling":[{"msid":81523351,"title":"Ransomware attack on Pimpri Chinchwad Smart City servers managed by Tech Mahindra","entity_type":"ARTICLE","link":"\/news\/ransomware-attack-on-pimpri-chinchwad-smart-city-servers-managed-by-tech-mahindra\/81523351","category_name":null,"category_name_seo":"telecomnews"}],"related_content":[],"msid":81523393,"entity_type":"ARTICLE","title":"In a second win, tax-exempt status of Tata Trusts upheld","synopsis":"The Mumbai bench of the ITAT rejected the income tax department\u2019s claims that the trusts had violated laws related to charitable trusts by holding shares of Tata Sons.","titleseo":"telecomnews\/in-a-second-win-tax-exempt-status-of-tata-trusts-upheld","status":"ACTIVE","authors":[],"Alttitle":{"minfo":""},"artag":"ET Bureau","artdate":"2021-03-16 08:45:54","lastupd":"2021-03-16 08:45:54","breadcrumbTags":["Tata Trusts","Tata Sons","Tata Trusts tax exemption","Sir Ratan Tata Trust","policy"],"secinfo":{"seolocation":"telecomnews\/in-a-second-win-tax-exempt-status-of-tata-trusts-upheld"}}" data-authors="[" "]" data-category-name="" data-category_id="" data-date="2021-03-16" data-index="article_1">

孟买的长椅上的ITAT拒绝了所得税部门声称信托违反了相关法律慈善信托基金持有的股票塔塔的儿子。

这是法庭第二执政的塔塔信托-Ratan Tata先生的信任塔塔,塔塔先生Dorabji信任和JRD信任。该裁决是评估2015年- 16所示。2020年12月,塔塔的法庭裁定赞成倚靠一个相同的案例评估2014年- 15。

在其2020年12月,法庭注意到,“只要股票语料库的一部分,6月1日,1973年,或股票收到的吸积股票被认为是语料库的一部分,13节的规定(1)(c)不会发挥作用。”

订单是塔塔的赢得信任的战斗保持免税地位。法庭的观察股票所有权可能影响情况下,信托公司对税务部门的注销登记。

2016年,所得税的专员(免)(CIT-E)威胁要颠覆了几十年来的所有权Tata Sons由信托公司宣称这种持股法律违反了所得税。

根据2020年12月的裁决,争端的起源CIT-E躺在2016订单,这拒绝给予免税Ratan Tata先生的信任,塔塔先生Dorabji信任和JRD信任评估官,称之为错误和偏见的收入和利益的需要修订。这件事是否是返回的申请AY14-15 Dorabji爵士(2013 - 14)财政年度的塔塔的信任。

塔塔信托上诉法庭,CIT-E否认这一说法。

信托公司否认他们违反了所得税法律通过沉溺于“禁止的投资模式”——也就是说,Tata Sons股票的所有权。他们指出,免税已经在前几年,所有持有的股票在FY13-14持有的信托基金在6月1日之前,1973年,后续增加语料库是只有通过分红的股票。它进一步表示,所有他们持有的股票作为语料库和这些股票的股息收入被塔塔信托慈善的对象。

根据阿施施K辛格,律师事务所的管理合伙人顶点合法的,每一个评估需要单独考虑。

“开办的推理是,因为挑战的修订订单已经决定支持塔塔的信任评估年2014 - 15,类似的订单需要通过后续年以及事实是相同的,”辛格说。

Mumbai: The Income Tax Appellate Tribunal has upheld the tax-exempt status of the Tata Trusts<\/a> and allowed their appeals against a revenue department order seeking to re-examine their tax assessments.

The Mumbai bench of the ITAT rejected the income tax department’s claims that the trusts had violated laws related to charitable trusts by holding shares of Tata Sons<\/a>.

This is the tribunal’s second ruling in favour of the Tata Trusts – Sir Ratan Tata Trust<\/a>, Sir Dorabji Tata Trust and the JRD Tata Trust. The ruling was for the assessment year 2015-16. In December 2020, the tribunal ruled in favour of the Tata Trusts in an identical case for assessment year 2014-15.

“Since the revision order under Section 263 of the Act for the assessment year 2015-16 was passed on identical facts and circumstances prevailing for the year 2014-15 in all the three trusts... all the three appeals... shall apply mutatis mutandis to this assessment year also,” a two-member bench of the ITAT said in its order of March 8, which was made available on Monday. “The operative portion of the said order of the tribunal is not reproduced herein for the sake of brevity. Accordingly, the grounds raised by the assessee are allowed.”

In its December 2020 order, the tribunal observed that “as long as the shares are part of the corpus, as on June 1, 1973, or the shares are received as an accretion to the shares being held to be part of the corpus, the provisions of Section 13(1)(c) will not come into play.”

The order was a win for Tata Trusts in its battle to retain tax-exempt status. The tribunal’s observations on share ownership are likely to influence a case where the trusts challenged the tax department’s cancellation of their registrations.

In 2016, the commissioner of income tax (exemption) (CIT-E) had threatened to upend the decades-old ownership of Tata Sons by the trusts by alleging that such shareholdings violated income tax laws.

As per the December 2020 ruling, the genesis of the dispute lay in the 2016 order by the CIT-E, which rejected the grant of tax exemption to Sir Ratan Tata Trust, Sir Dorabji Trust and the JRD Tata Trust by the assessing officer, calling it erroneous and prejudicial to the interests of revenue and requiring revision. The matter pertained to the returns filed for AY14-15 (financial year 2013-14) by Sir Dorabji Tata Trust.

The Tata Trusts appealed to the tribunal, denying the claims of the CIT-E.

The Trusts denied that they had violated income tax laws by indulging in “prohibited modes of investment” – that is, ownership of Tata Sons shares. They pointed out that tax exemption had been granted in previous years and that all the shares held in FY13-14 were held by the trusts before June 1, 1973, and subsequent additions to the corpus were only through bonus shares. It further stated that all the shares were held by them as corpus and the dividend income from these shares was used by the Tata Trusts for its charitable objects.

According to Ashish K Singh, managing partner of law firm Capstone Legal, each assessment year is required to be considered separately.

“The reasoning given by ITAT is that since the revision order which was challenged has been decided in favour of Tata Trusts for the assessment year in 2014-15, similar order is required to be passed for the subsequent year as well as the facts are identical,” said Singh.

<\/p><\/body>","next_sibling":[{"msid":81523351,"title":"Ransomware attack on Pimpri Chinchwad Smart City servers managed by Tech Mahindra","entity_type":"ARTICLE","link":"\/news\/ransomware-attack-on-pimpri-chinchwad-smart-city-servers-managed-by-tech-mahindra\/81523351","category_name":null,"category_name_seo":"telecomnews"}],"related_content":[],"msid":81523393,"entity_type":"ARTICLE","title":"In a second win, tax-exempt status of Tata Trusts upheld","synopsis":"The Mumbai bench of the ITAT rejected the income tax department\u2019s claims that the trusts had violated laws related to charitable trusts by holding shares of Tata Sons.","titleseo":"telecomnews\/in-a-second-win-tax-exempt-status-of-tata-trusts-upheld","status":"ACTIVE","authors":[],"Alttitle":{"minfo":""},"artag":"ET Bureau","artdate":"2021-03-16 08:45:54","lastupd":"2021-03-16 08:45:54","breadcrumbTags":["Tata Trusts","Tata Sons","Tata Trusts tax exemption","Sir Ratan Tata Trust","policy"],"secinfo":{"seolocation":"telecomnews\/in-a-second-win-tax-exempt-status-of-tata-trusts-upheld"}}" data-news_link="//www.iser-br.com/news/in-a-second-win-tax-exempt-status-of-tata-trusts-upheld/81523393">

评论

现在评论 阅读评论(1)所有评论

找到这个评论进攻?

下面选择你的理由并单击submit按钮。这将提醒我们的版主采取行动