独家

IT服务公司清醒FY19增长前景

投资者还将增加在数字支出和预算分配的项目。Saluja补充说,他预计公司将开始“保守的一面FY19收入增长指导”。

投资者还将增加在数字支出和预算分配的项目。Saluja补充说,他预计公司将开始“保守的一面FY19收入增长指导”。

印度信息技术服务公司可能会谨慎而预测增长FY19,尽管分析师预计比FY18更好的增长,随着问题的支出由银行和金融服务客户依然存在。

印度信息技术服务公司可能会谨慎而预测增长FY19,尽管分析师预计比FY18更好的增长,随着问题的支出由银行和金融服务客户依然存在。

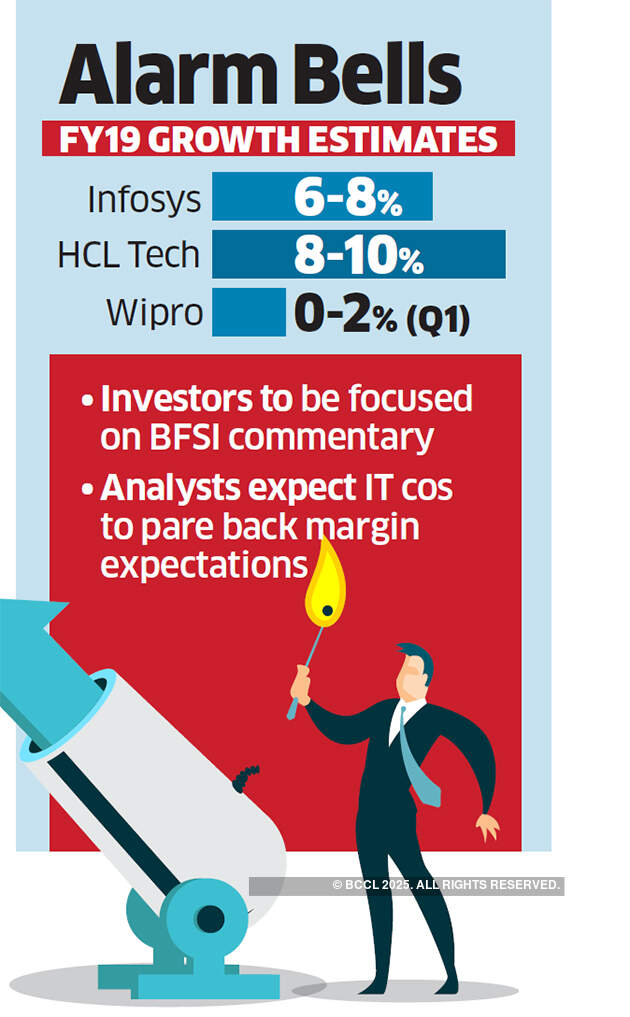

Indian IT services<\/a> firms are likely to be cautious while forecasting growth<\/a> for FY19, even as analysts expect better growth than in FY18, as questions over the spending by banking and financial services clients remain.

Indian IT services<\/a> firms are likely to be cautious while forecasting growth<\/a> for FY19, even as analysts expect better growth than in FY18, as questions over the spending by banking and financial services clients remain.

不到16年经验的官员受到缺口,而高级年级有一个长期的经验。凹陷水平相当于政府部门的联合秘书,虽然缺口是在主管级别。